About this review

The best condo insurance in Florida is not one company for every owner. A strong choice depends on your condo association’s master policy, what you must insure inside the unit, whether private-market coverage is available, how much deductible risk you can handle, whether flood coverage needs to be handled separately, and whether you prefer a local agent, a digital-first process, or a fallback option when regular private coverage is limited.

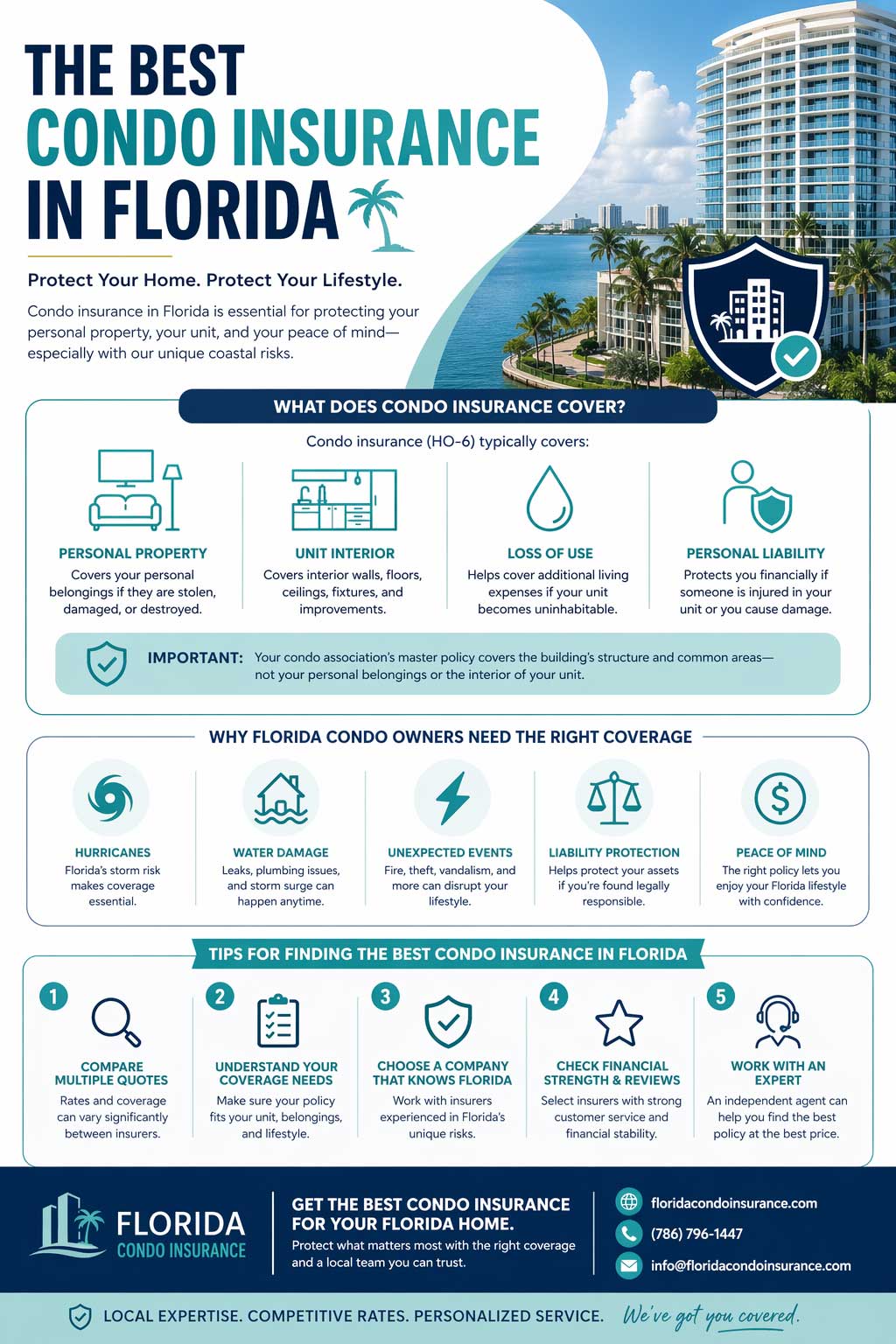

Condo insurance is different from standard homeowners insurance because the association and the unit owner usually insure different parts of the property. The Florida Office of Insurance Regulation describes HO-6 condo insurance as “walls-in” coverage for the interior of the structure while the condo association’s master policy covers the exterior structure and common areas. FLOIR also notes that HO-6 policies generally provide coverage for building property, personal property, personal liability, and loss of use, and that HO-6 usually does not cover flooding. [1]

- Best fallback option to understand: Citizens, when private-market coverage is limited or unavailable.

- Best traditional shopping path to compare: State Farm, if you want an agent-supported process and a familiar national carrier.

- Best digital-first option to compare: Kin, if you prefer an online-first Florida condo insurance experience.

- Best comparison method: independent agent or multi-carrier shopping when you need several private-market quotes normalized by limits and deductibles.

- Best overall approach: choose the company and policy that match your association documents, HO-6 needs, deductible comfort, loss assessment exposure, and flood questions.

How this Florida condo insurance comparison was built

This page does not name one universal winner because Florida condo insurance depends heavily on the building, association documents, underwriting availability, lender requirements, and the unit owner’s risk tolerance. Instead, it compares useful shopping paths for different situations: Citizens for market-access concerns, State Farm for agent-supported shopping, Kin for digital-first comparison, and independent or multi-carrier shopping for broader private-market review.

Best condo insurance options to compare in Florida

The options below are not a universal ranking and should not be treated as personalized insurance advice. They are useful comparison categories for common Florida condo-owner situations. A company that works well for one owner may not be available or appropriate for another owner’s building, lender, location, deductible preference, or association setup.

Citizens: best to understand when private options are limited

Citizens is important in Florida because some condo owners may have limited private-market options. Citizens says its personal residential policies are designed for homeowners and renters across Florida who cannot find coverage in the private market, including people who live in condominiums. Citizens also describes condominium unit owner policies as available to condominium-unit owners who live in the unit, covering certain interior features, personal property, additional living expenses, and liability, but not the exterior of the condominium building. [2]

Why compare Citizens

- Private-market options are limited.

- Your building or location is harder to place.

- You need a fallback option while reviewing alternatives.

- You want to understand whether Citizens or a private carrier gives better fit.

What to check carefully

- Eligibility and quote availability.

- Interior coverage limits.

- Wind-only or multi-peril structure.

- Deductibles and assessment exposure.

- Private-market offers that may be available.

State Farm: best to compare for agent-supported shopping

State Farm can be worth comparing if you prefer a traditional insurer with agent support. Its condo quote materials tell shoppers to refer to current condominium unitowners coverage and deductibles, review condo association bylaws, and understand what the master association policy insures before starting a quote. That process matters in Florida because the association-versus-owner split can change what your HO-6 policy should cover. [3]

Why compare State Farm

- You want agent help reviewing quote assumptions.

- You prefer a traditional shopping process.

- You want help checking bylaws and association responsibilities.

- You want to compare a national carrier against Florida-focused options.

What to check carefully

- Whether your unit qualifies.

- Whether online quoting is available for your situation.

- Coverage A and Coverage C assumptions.

- Deductibles and endorsements.

- Agent support after the quote, not just before purchase.

Kin: best to compare for a digital-first Florida condo experience

Kin can be worth comparing if you prefer an online-first quote process. Kin describes condo insurance as an HO-6 policy that covers the unit interior from the walls in, including personal property, while the condo association’s master policy covers the exterior and common areas. Kin also says condo insurance does not cover damage caused by external flooding and rising waters, which is an important reminder for Florida condo owners. [4]

Why compare Kin

- You prefer a digital-first quote experience.

- You want Florida-focused condo insurance messaging.

- You want to compare customizable HO-6 options.

- You want online access before speaking with someone.

What to check carefully

- Whether your building and ZIP code are eligible.

- Flood coverage or separate flood policy needs.

- Windstorm details and deductibles.

- Water backup and optional endorsements.

- Final policy terms before purchase.

Independent agents and multi-carrier comparisons

An independent agent or multi-carrier comparison can be useful when you want several private-market quotes instead of one company’s offer. This can be especially helpful if your building has unusual underwriting details, if you are comparing coastal and inland options, or if you need help normalizing deductibles, endorsements, exclusions, and quote assumptions.

Multi-carrier shopping is strongest when you compare each quote with the same Coverage A limit, personal property limit, liability limit, loss assessment limit, deductible structure, water backup assumption, replacement cost assumption, and flood insurance question. Without that normalization, the lowest premium may simply be the weakest quote.

Affordable Florida condo insurance: what it really means

Affordable Florida condo insurance should mean good value, not just the lowest first premium. A cheap quote can become expensive if it uses weak personal property limits, a high hurricane deductible, limited loss assessment protection, actual cash value instead of replacement cost, or no clear explanation of flood exposure.

What the best Florida condo insurance quote should include

A strong quote should make it easy to see what is covered, what is optional, and what remains outside the policy. For Florida condo owners, the quote should be checked against the association documents and the actual unit, not just compared against another premium.

How to compare condo insurance companies fairly

- Review your association certificate of insurance, declaration, bylaws, master-policy summary, and deductible schedule before requesting quotes.

- Keep interior building property, personal property, liability, loss of use, and loss assessment assumptions consistent.

- Compare hurricane, wind, and all-other-perils deductibles carefully.

- Ask whether loss assessment coverage is included and whether higher limits are available.

- Ask whether water backup, equipment breakdown, replacement cost, or special limits for valuables require endorsements.

- Ask how the quote handles flood exposure and whether separate flood insurance is needed.

- Compare claims support, agent access, digital tools, billing, and renewal process before choosing.

A Florida warning: best does not mean flood is solved

A condo insurer can still be a poor fit if the quote leaves flood exposure unresolved. FLOIR states that HO-6 usually does not cover flooding, and Kin’s condo insurance materials also state that condo insurance does not cover damage caused by external flooding and rising waters. Florida condo owners should ask whether the association carries flood coverage, whether contents flood coverage is needed, and whether the lender requires flood insurance. [1] [4]

- What exactly am I insuring inside the unit?

- What does this quote assume my association already covers?

- Which deductible would I actually owe after a covered loss?

- What protections are standard, and what requires an endorsement?

- What does this quote not solve for a Florida condo owner?

- Does the company clearly explain flood, wind, water backup, and loss assessment limitations?

- Can I review a sample declarations page before deciding?

Best condo insurance by Florida owner type

Common mistakes when choosing the best condo insurance in Florida

- Choosing the cheapest quote without comparing the limits.

- Assuming the association master policy covers everything inside the unit.

- Not checking whether flood insurance is separate.

- Ignoring loss assessment coverage or leaving the lowest limit without review.

- Comparing quotes with different deductibles and calling one “cheaper.”

- Not asking about replacement cost versus actual cash value.

- Ignoring water backup, special limits, and endorsements.

- Waiting until closing or renewal week to request association documents.

- Assuming a company is available for every Florida condo building.

- Assuming “best company” matters more than “best fit for this unit.”

Useful next steps

To understand the policy form before comparing companies, review our Florida HO6 Insurance guide. For the broader statewide framework, see our Condo Insurance in Florida guide. If price is your main concern, review our Cheapest Condo Insurance in Florida guide. When you are ready to compare actual offers, continue with our Florida Condo Insurance Quotes page.

You can also review broader insurer information through our Florida Condo Insurance Companies page, check statewide rules in our Florida Condo Insurance Requirements guide, or browse local pages from our Florida condo insurance city guide.

FAQ: best condo insurance in Florida

What is the best condo insurance company in Florida?

There is no single best company for every owner. The best option depends on your building, association policy, private-market availability, unit-owner coverage needs, deductible comfort, flood exposure, and service preference.

Is Citizens the best condo insurance option in Florida?

Citizens can be important when private-market coverage is limited, but it should not automatically be treated as the best option for every owner. Compare Citizens against any available private-market offers and review the coverage details carefully.

Should I choose the cheapest Florida condo insurance quote?

Not without comparing the coverage. A cheaper quote may have lower personal property limits, higher deductibles, weaker loss assessment coverage, actual cash value claim settlement, or missing endorsements.

Is affordable Florida condo insurance the same as cheap condo insurance?

Not always. Affordable condo insurance should balance price with coverage quality, deductibles, loss assessment protection, personal property limits, liability limits, and Florida-specific risks such as flood and wind exposure.

Does condo insurance in Florida cover flood damage?

Standard HO-6 condo insurance usually does not cover flood damage. Florida condo owners should review flood insurance separately and ask whether the association carries flood coverage for the building.

What should I compare between condo insurance companies?

Compare interior property limits, personal property limits, liability limits, loss of use, loss assessment, deductibles, exclusions, endorsements, flood handling, claim support, agent access, billing, and renewal process.

Do I need my condo association documents before comparing companies?

Yes. Your association certificate of insurance, declaration, bylaws, master policy summary, and deductible information help determine what your own policy should cover.

Is Kin or State Farm better for Florida condo insurance?

It depends on your situation. Kin may be worth comparing if you prefer a digital-first quote process, while State Farm may be worth comparing if you prefer agent-supported shopping. Availability, price, deductibles, endorsements, flood handling, and final policy terms should decide the better fit.

Bottom line

The best condo insurance in Florida is the policy and company combination that fits your actual unit, building, association documents, deductible comfort, and coverage gaps. The most affordable choice is usually the one that gives you the best value for those needs, not simply the lowest initial quote.

For some owners, Citizens may matter because private options are limited. For others, State Farm, Kin, or a multi-carrier comparison may be a better place to start. The safest way to compare is to keep the limits and deductibles consistent, review what the association already insures, ask about flood and loss assessment separately, and choose the company that leaves the fewest surprises after a claim.

Compare Florida condo insurance quotes using the same limits, deductibles, personal property assumptions, liability limits, loss assessment needs, and flood questions so you can find the best value, not just the lowest price.

Compare Florida Condo Insurance QuotesReferences

- Florida Office of Insurance Regulation, “Homeowners Insurance.” Source · ↩

- Citizens Property Insurance Corporation, “Residential Policies.” Source · ↩

- State Farm, “Condo Insurance Quote.” Source · ↩

- Kin Insurance, “Condo Insurance.” Source · ↩

- Florida Statutes, Section 627.714, “Residential condominium unit owner coverage; loss assessment coverage required.” Source · ↩