About this review

Miami condo insurance is not just a local version of a standard homeowners policy. A condo owner in Miami usually has to understand how the association’s master policy works, what the individual unit-owner policy is supposed to protect, and how local risks such as flood exposure, storm surge, hurricane deductibles, high-rise construction, and association assessments can affect the real value of a quote.

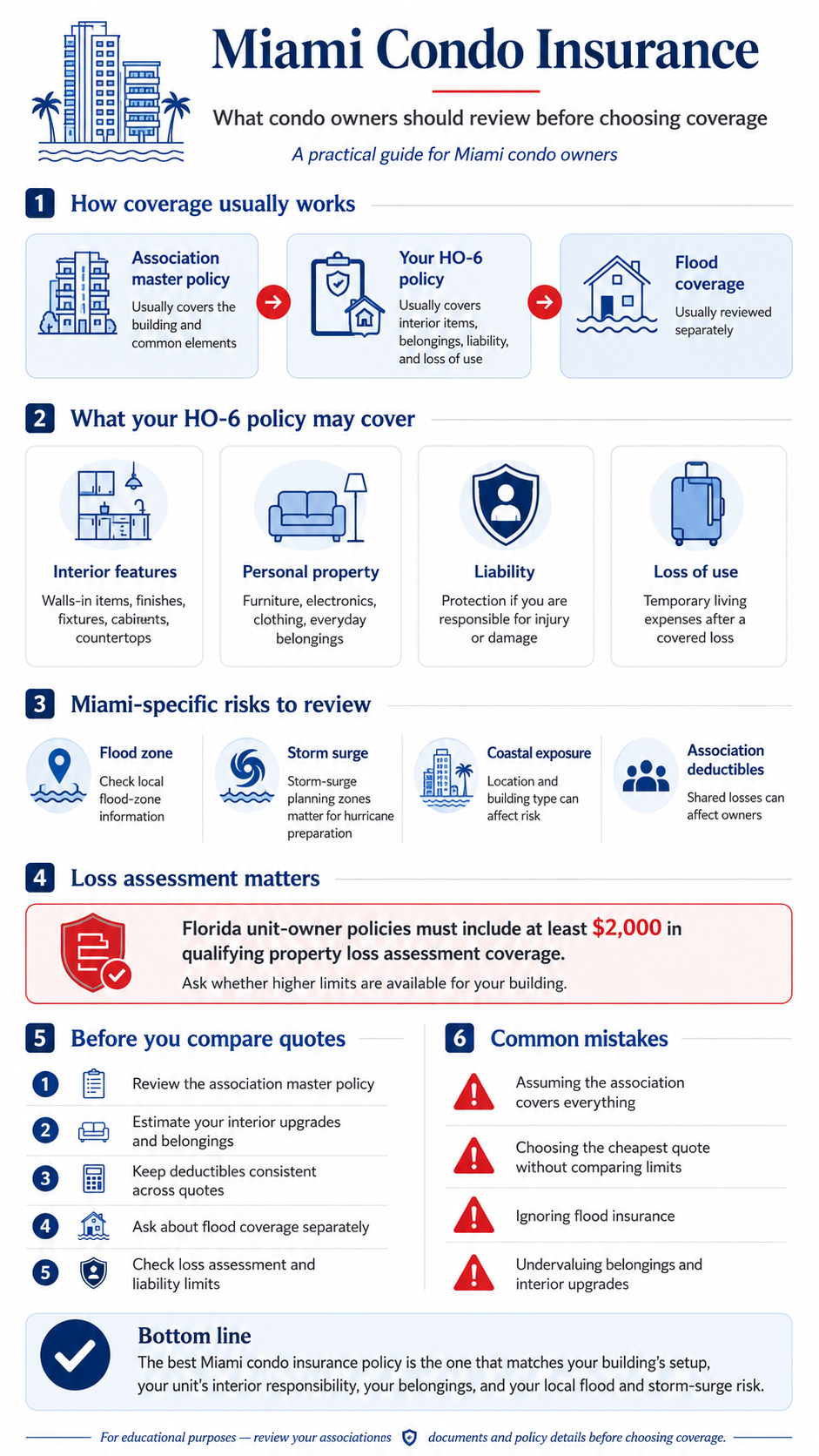

The most useful way to compare Miami condo insurance quotes is to separate the decision into two parts. First, review what the condominium association insures for the building and common elements. Second, review what you personally need to protect inside the unit, including interior finishes, belongings, liability, temporary living expenses, flood-related questions, lender requirements, and possible loss assessment exposure. That approach gives Miami owners a better foundation than comparing premiums without knowing what each quote actually assumes.

- Miami condo owners usually need to review both the association master policy and their own HO-6 unit-owner policy.

- Florida HO-6 condo coverage is commonly described as “walls-in” coverage for the interior side of condo ownership.

- Flood insurance is usually a separate issue and should not be assumed to be included in a standard condo policy.

- Miami-Dade flood zones and storm-surge planning zones are different tools, and both can matter when reviewing risk.

- Loss assessment coverage deserves special attention because shared association losses and deductibles can become expensive after a major event.

- Miami buyers should gather association insurance documents before closing so quote limits match the building and lender requirements.

- Brickell, Downtown, Edgewater, Miami Beach, Coconut Grove, Coral Gables, and Sunny Isles condos can raise different flood, wind, high-rise, and association-deductible questions.

Compare Miami condo insurance options by ZIP code, building type, association requirements, flood exposure, personal property limits, loss assessment needs, and deductible preferences.

Compare Miami Condo Insurance Quotes

Why Miami condo insurance needs a local approach

Miami condo ownership often involves risks and questions that are more specific than a simple statewide condo insurance explanation. A unit in Brickell, Downtown Miami, Edgewater, Miami Beach, Coconut Grove, Coral Gables, Sunny Isles, or another Miami-area market may involve different building age, elevation, association insurance limits, flood exposure, lender expectations, and interior improvement values. The policy should be built around the unit and the building, not only around a ZIP code.

Miami-Dade County says FEMA’s digital flood hazard maps reflect current flood risks for the county and are used when determining flood insurance policy rates. The county also tells residents and businesses to use the maps to better understand potential flood risk and identify steps they may need to take to protect property. [1]

Miami condo insurance by area and building type

A useful Miami condo insurance quote should reflect more than the word “Miami.” Building height, coastal exposure, bayfront location, association deductible structure, unit upgrades, occupancy type, and lender instructions can all change the questions you should ask before choosing coverage.

Association master policy vs. your Miami HO-6 policy

Florida condo owners should not assume that the association’s insurance solves everything. Florida Statute 718.111 says a residential condominium association must use its best efforts to maintain adequate property insurance for association property, common elements, and the condominium property the association must insure. The same statute also explains that association coverage must exclude personal property within the unit and several interior items such as floor, wall, and ceiling coverings, electrical fixtures, appliances, water heaters, built-in cabinets, countertops, and window treatments that are located within the unit and serve only that unit. Such property and the insurance on it are the unit owner’s responsibility. [2]

That is why a Miami condo owner should read the association documents before choosing limits. If the unit has upgraded flooring, custom closets, built-in cabinets, renovated bathrooms, upgraded lighting, or higher-value appliances, the difference between association coverage and unit-owner responsibility can matter after a covered loss.

What HO-6 condo insurance can cover in Miami

The Florida Office of Insurance Regulation describes HO-6 condo insurance as coverage for condominiums and notes that it is often called “walls-in” coverage because it covers the interior of the structure while the condo association’s master policy covers the exterior structure and common areas. FLOIR also states that HO-6 policies generally provide coverage for building property, personal property, personal liability, and loss of use. [3]

Interior building property

This can involve the parts of the unit that are your responsibility, such as certain interior finishes, built-ins, fixtures, cabinets, countertops, and improvements.

Personal property

Furniture, electronics, clothing, décor, kitchen items, small appliances, and everyday belongings should be estimated realistically before choosing a limit.

Personal liability

Liability coverage may help if you are responsible for injury or property damage involving someone else.

Loss of use

Loss of use can help with additional living expenses if a covered loss makes your condo temporarily unlivable.

Flood insurance and storm surge in Miami

Flood is one of the most important issues for Miami condo owners because standard condo insurance and flood insurance are not the same thing. FLOIR states that HO-6 policies usually do not cover flooding and that additional coverage needs to be purchased if flood insurance is desired. FloodSmart also explains that most homeowners and renters insurance does not cover flood damage, and that NFIP flood policies are available for homeowners, including people who own condominiums and townhouses in participating NFIP communities. [4] [5]

Miami-Dade County also explains that storm surge is the greatest threat to life and property from a hurricane and that storm-surge planning zones are used for evacuation decisions. The county says these zones are separate from flood zones, which means Miami condo owners should not treat a flood-zone check and a storm-surge planning check as the same thing. [6]

- Check the unit’s flood zone before assuming the standard HO-6 policy is enough.

- Review whether the association carries flood coverage for the building.

- Ask whether you need contents flood coverage for belongings inside the unit.

- Check your storm-surge planning zone separately from your flood zone.

- Confirm any flood requirements tied to your mortgage lender.

Loss assessment coverage matters in Miami condo buildings

Loss assessment coverage can matter when a condominium association assesses owners after certain shared property losses, association deductibles, or covered building-level events. Florida Statute 627.714 states that unit owner residential property policies issued or renewed on or after July 1, 2010 must include at least $2,000 in property loss assessment coverage for qualifying assessments made as a result of the same direct loss to property, when the loss is of the type covered by the unit owner’s residential property insurance policy. [7]

The minimum amount is not automatically the right amount for every Miami condo owner. A large coastal building, a high association deductible, older construction, limited reserves, or a major covered loss can make assessment risk more serious. Owners should ask whether higher loss assessment limits are available, what deductible applies, and which types of assessments are excluded.

- What is the policy’s loss assessment limit?

- Can the limit be increased?

- Does the coverage apply to association deductibles after a covered property loss?

- Is there a separate deductible for loss assessment coverage?

- Which assessments are not covered?

Miami condo quote factors to compare side by side

The strongest Miami condo quote is not always the quote with the lowest first premium. Compare each option using the same assumptions so one policy is not cheaper only because it has weaker limits, higher deductibles, or missing coverage questions.

Miami condo insurance before closing

Miami condo buyers should not wait until the last week before closing to review insurance. A lender or title company may request proof of coverage, mortgagee wording, minimum limits, flood information, or confirmation that the association carries certain coverage. The fastest way to avoid delays is to gather documents before choosing an HO-6 quote.

- Ask the association or property manager for the certificate of insurance.

- Review the declaration, bylaws, and deductible information before setting HO-6 limits.

- Confirm whether the lender requires flood insurance or specific mortgagee wording.

- Estimate personal property and interior upgrades before accepting a low quote.

- Ask about loss assessment coverage and whether higher limits are available.

Documents to review before comparing Miami condo insurance quotes

A Miami condo quote is much easier to evaluate when you know what the building already insures and what you personally need to cover. Before choosing a policy, ask for the association’s insurance certificate, declarations page if available, bylaws, condominium declaration, budget or reserve information, deductible information, and any lender-specific insurance requirements.

How to compare Miami condo insurance quotes

Many Miami condo owners compare quotes by premium first, but that can be misleading. A cheaper quote may simply use lower personal property limits, weaker loss assessment coverage, higher deductibles, limited water backup protection, or a different assumption about what is covered inside the unit. For a fair comparison, keep the major limits and deductibles as close as possible before deciding which option is better.

For broader statewide context, review our Condo Insurance in Florida guide. For a policy-type explanation, use our Florida HO6 Insurance page. For lender, association, and owner-responsibility questions, review Florida Condo Insurance Requirements. Once you are ready to compare options, continue with our Florida Condo Insurance Quotes guide.

- Review the association master policy before choosing your HO-6 limits.

- Estimate your personal property and interior improvements separately.

- Compare hurricane, wind, and all-other-perils deductibles carefully.

- Ask about loss assessment, water backup, liability, and loss of use.

- Review flood insurance separately from the standard condo policy.

- Check lender requirements before accepting the lowest premium.

Common mistakes Miami condo owners should avoid

- Assuming the association’s master policy covers everything inside the condo.

- Ignoring flood insurance because the unit is above ground level.

- Confusing flood zones with storm-surge planning zones.

- Choosing the cheapest quote without comparing deductibles and limits.

- Forgetting to review loss assessment coverage.

- Undervaluing personal belongings and interior upgrades.

- Waiting until closing or renewal week to ask for association insurance documents.

- Assuming every Miami condo building creates the same insurance need.

Where to go next

If price is your main concern, compare this page with our Cheapest Condo Insurance in Florida guide. If you want a broader value comparison, use Best Condo Insurance in Florida. If you are deciding between carriers or agency options, review Florida Condo Insurance Companies before requesting quotes.

FAQ: Miami condo insurance

Is condo insurance required in Miami?

Many Miami condo owners need HO-6 coverage because of lender requirements, association documents, or practical financial protection. Even when a specific owner is not forced to buy a policy in the same way as another owner, coverage can still be important for interior property, belongings, liability, loss of use, and loss assessment exposure.

Does the condo association policy cover my Miami unit?

The association policy may cover building-level property and common elements, but it usually does not cover your personal belongings, liability, temporary living expenses, or many interior items that serve only your unit. Review the association documents before deciding your limits.

Does Miami condo insurance cover flood damage?

Standard HO-6 condo insurance usually does not cover flood damage. Miami condo owners should review flood coverage separately, check whether the association carries flood insurance for the building, and ask whether they need contents flood coverage for their personal property.

What is loss assessment coverage for a Miami condo owner?

Loss assessment coverage can help when a condo association assesses unit owners after certain covered property losses. Florida requires at least $2,000 in qualifying property loss assessment coverage in unit owner residential property policies, but some owners may want to ask about higher limits.

How much Miami condo insurance should I buy?

The right amount depends on your association’s insurance setup, your interior responsibility, your personal property value, your deductible comfort, your loss assessment exposure, your lender requirements, and whether you need separate flood coverage.

What should I prepare before closing on a Miami condo?

Ask for the association certificate of insurance, master policy deductible details, condo declaration, bylaws, lender insurance instructions, flood-zone information, and a list of interior upgrades before accepting a quote. This helps the HO-6 policy match the building, lender, and unit details.

Should Miami Beach and Brickell condo owners compare coverage differently?

They should ask more detailed location and building questions. A coastal or high-rise condo may raise different flood, wind, deductible, association, and lender concerns than a smaller inland building. The policy should reflect the actual unit and building, not only the city name.

Bottom line

Miami condo insurance works best when it is treated as a building-specific and unit-specific decision. The right policy should reflect what the association insures, what you are responsible for inside the unit, how much your belongings and upgrades are worth, whether loss assessment coverage is strong enough, and whether flood insurance needs to be handled separately.

A low premium may look attractive, but the better question is whether the quote would still make sense after a real Miami loss scenario. Review the documents, compare limits carefully, ask the flood question early, and choose coverage that fits the unit instead of relying only on the cheapest number.

Compare Miami condo insurance options after you understand your association policy, HO-6 needs, deductible exposure, flood question, lender requirements, and loss assessment risk.

Compare Miami Condo Insurance QuotesReferences

- Miami-Dade County, “Flood Zone Maps.” Source · ↩

- Florida Statutes, Section 718.111, “The association — Insurance.” Source · ↩

- Florida Office of Insurance Regulation, “Homeowners Insurance — HO-6 Condo Form.” Source · ↩

- Florida Office of Insurance Regulation, “Homeowners Insurance — HO-6 flood note.” Source · ↩

- FEMA FloodSmart, “What you need to know about buying flood insurance.” Source · ↩

- Miami-Dade County, “Storm Surge Planning Zones.” Source · ↩

- Florida Statutes, Section 627.714, “Residential condominium unit owner coverage; loss assessment coverage required.” Source · ↩