About this review

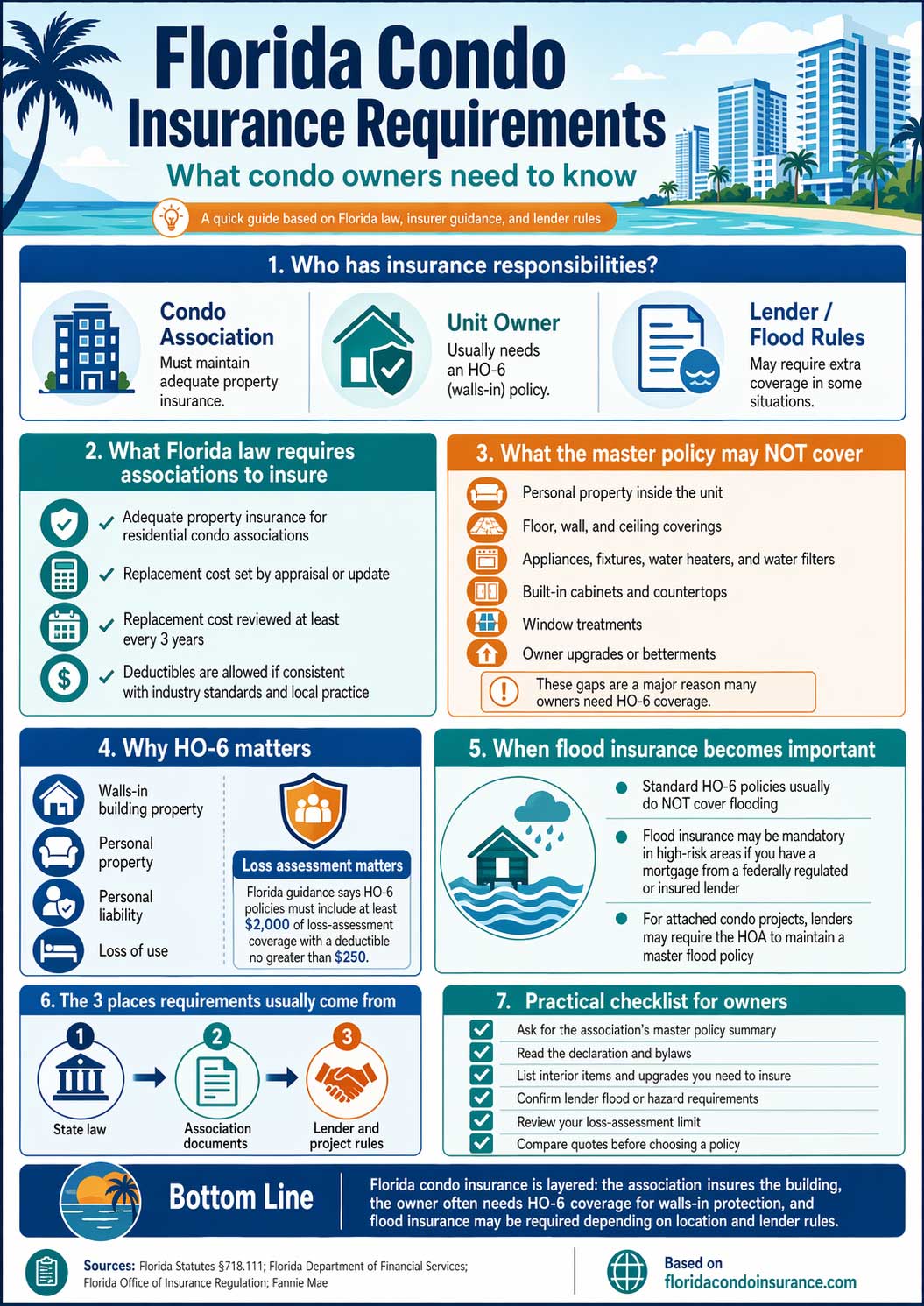

Florida condo insurance requirements are not always a one-line answer. Some requirements are imposed on the condominium association by state law, while others affect the unit owner through lender rules, flood-zone rules, association documents, or the simple reality that the master policy does not insure everything inside the unit.[1][2][3]

The practical question for most buyers and owners is not just “Is insurance required?” but “What coverage am I personally expected to carry?” That answer usually starts with the association’s master policy, then moves to your condo insurance in Florida needs as an individual owner.

The association and the unit owner usually have different insurance responsibilities

Florida law directly requires the condominium association to maintain adequate property insurance. For the unit owner, the usual requirement is to carry an HO-6 policy or similar walls-in coverage when needed to protect personal property, interior items, liability, loss assessment, and any gaps left by the master policy.

Lender-driven rules

Coverage gaps matter

Florida law says every residential condominium association must have adequate property insurance, and replacement cost must be determined at least once every three years.[1]

Florida DFS says condo unit owners need the Condominium Unit-Owners Form, commonly called HO-6, which primarily covers personal property and liability and may also cover some structure-related items.[2]

What Florida law requires the condominium association to insure

The clearest legal requirement in Florida is on the association side. Section 718.111 says every residential condominium association must have adequate property insurance. The statute also says the amount of adequate coverage may be based on replacement cost determined by an independent insurance appraisal or an update of a previous appraisal, and that replacement cost must be determined at least once every three years.[1]

What the association’s policy does not necessarily cover for you

This is where many Florida condo owners get confused. Florida’s condo statute says the association policy must exclude personal property within the unit and many interior items that only serve the unit. That is a big reason unit owners end up needing walls-in protection even when the association maintains a robust master policy.[1]

Interior items that often push owners toward HO-6 coverage

- Personal property inside the unit

- Floor, wall, and ceiling coverings

- Electrical fixtures, appliances, water heaters, and water filters

- Built-in cabinets and countertops

- Window treatments

- Later upgrades or betterments that belong to the unit owner

Why many Florida condo owners still need HO-6 insurance

Florida DFS says condo unit owners need the Condominium Unit-Owners Form, also called HO-6. FLOIR describes condo insurance as “walls-in” coverage and says HO-6 will generally provide coverage for building property, personal property, personal liability, and loss of use.[2][3]

Loss assessment is one of the most overlooked requirements

Florida DFS says condo unit-owner policies provide loss assessment coverage, and the homeowners toolkit says an HO-6 policy must provide at least $2,000 of loss-assessment coverage with a deductible no greater than $250. This matters because associations may assess owners for covered damage to common property or for costs the association cannot fully absorb.[2][4]

When flood insurance becomes a real requirement

FLOIR says HO-6 usually does not cover flooding and that additional coverage must be purchased if flood insurance is desired. FLOIR also says flood insurance is required in high-risk areas for homes with mortgages from federally regulated or insured lenders. For attached condo projects, Fannie Mae says that when flood insurance is required, the lender must verify that the HOA maintains a master flood insurance policy paid as a common expense.[3][5]

- Flood is not automatically part of a standard condo unit-owner policy.

- A mortgage in a high-risk flood area can make flood insurance mandatory.

- Some lenders may require flood coverage even outside the highest-risk zones.

- In attached condo projects, the project-level master flood policy can be a lender requirement.

The three places condo insurance requirements usually come from

1. State law

Florida law puts clear insurance duties on the condominium association and shapes what the master policy must and must not cover.[1]

2. Association documents

Your declaration, bylaws, and master policy details can determine where the owner’s responsibility starts inside the unit.

3. Lender and project rules

A mortgage lender may require hazard or flood coverage based on the loan, the location, and the type of condo project involved.[5]

Check your requirements, then compare your options

Once you know what the association insures, what your lender expects, and what the master policy excludes, you are in a much better position to review actual pricing and policy differences.

A practical checklist for Florida condo owners

- Ask for the association’s current master policy summary.

- Read your declaration or bylaws for insurance-related language.

- List the interior items and upgrades you would need to insure yourself.

- Confirm whether your lender has flood or hazard requirements.

- Review whether your policy includes sufficient loss-assessment protection.

- Compare more than one quote before deciding which policy structure fits best.

Bottom line

Florida condo insurance requirements usually work as a layered system. The association has statutory insurance duties, the unit owner often needs HO-6 or similar walls-in protection, and flood requirements can arise from lender and project rules rather than from one blanket statewide rule for every owner.[1][2][3][5]

The safest approach is to review your association documents, identify the interior items and exposures that belong to you, and then choose coverage that matches those responsibilities instead of assuming the master policy handles everything.

References

- The 2025 Florida Statutes, Section 718.111. Back to content ↑

- Florida Department of Financial Services, Homeowners Insurance Overview. Back to content ↑

- Florida Office of Insurance Regulation, Homeowners Insurance. Back to content ↑

- Florida Department of Financial Services, Homeowners Insurance Toolkit. Back to content ↑

- Fannie Mae, Flood Insurance Requirements for All Property Types. Back to content ↑

- Florida Office of Insurance Regulation, Flood Insurance. Back to content ↑

Florida Condo Insurance Editorial Team

Our editorial team creates Florida condo insurance content built around official state guidance, insurance education resources, and practical quote-comparison advice for condo owners and buyers.

Learn more about us or contact us with questions.